| This week, why the model that consumer-goods leaders have relied upon for decades is no longer creating steady growth. Plus, Nick Vlahos, CEO of The Honest Company, on consumer trends, building community, and a strategy for expanding into new markets. |

|

|

|

| For decades, global consumer-goods companies have prospered, building brands that have become household names. If you take a moment to think about the number of these products in your bathroom and kitchen, you’ll understand how the industry delivered one of the highest total returns to shareholders, at 15 percent, in the four decades before the 2008 financial crisis. |

| The same business model since WWII. Leading consumer-goods firms haven’t really changed their business model since the 1940s: they build brands, create innovative products, expand to developing markets, and partner with distribution channels, like grocers. This has created a virtuous cycle that generated steady growth and enabled further investment. |

| Consumer-goods growth has stalled out. Over the past decade, the sector has seen narrowing margins and worsening stock-market performance. The model’s no longer working. What’s changed? A number of trends, including the dominance of digital media and the expansion of small brands, are disrupting traditional methods of promoting brands and transforming sales channels. The COVID-19 crisis has accelerated many of these changes. |

| For instance, the use of digital has become increasingly important. With consumers spending more time at home as a result of the pandemic, e-commerce is surging in a way we haven’t seen before. According to our analysis, in the US alone there’s been a 15 to 30 percent jump in the number of people who do most of their shopping online. And, over the past five years, the revenues of e-marketplaces have grown 17 percent. |

| Image-conscious consumers. Many consumers, particularly millennial and Gen Z shoppers, care about their image and buy products as a means of self-expression. These self-conscious consumers seek brands that are ethical, sustainable, and make a positive difference in the world. To stay relevant, consumer-goods leaders need to imbue their brands with purpose and originality. |

| Another trend upending the industry. Small brands and private labels have seen an explosion of growth. In fact, leading brands in recent years have captured a paltry 25 percent of value growth in US Nielsen-covered channels, despite making up 50 percent of sales. Small brands acquired by major companies often perform better, but scaling up to $100 million in sales can remain a challenge. Anyone acquiring a smaller label would be wise to consider providing supply-chain training or other support to help the brand quickly scale up operations. |

| To thrive in this new era, industry leaders need a new strategy. For starters, businesses should embrace e-marketplaces and online sales channels. In addition, they will need to invest in relevance-led marketing, which must include a sharper targeting of consumers. They’ll also need to establish brands in developing markets, particularly in emerging Asia. Finally, companies should evolve their own operating models by digitizing wherever possible—enabling both rapid change and growth in productivity. |

|

|

|

| OFF THE CHARTS |

| Is brand loyalty dead? |

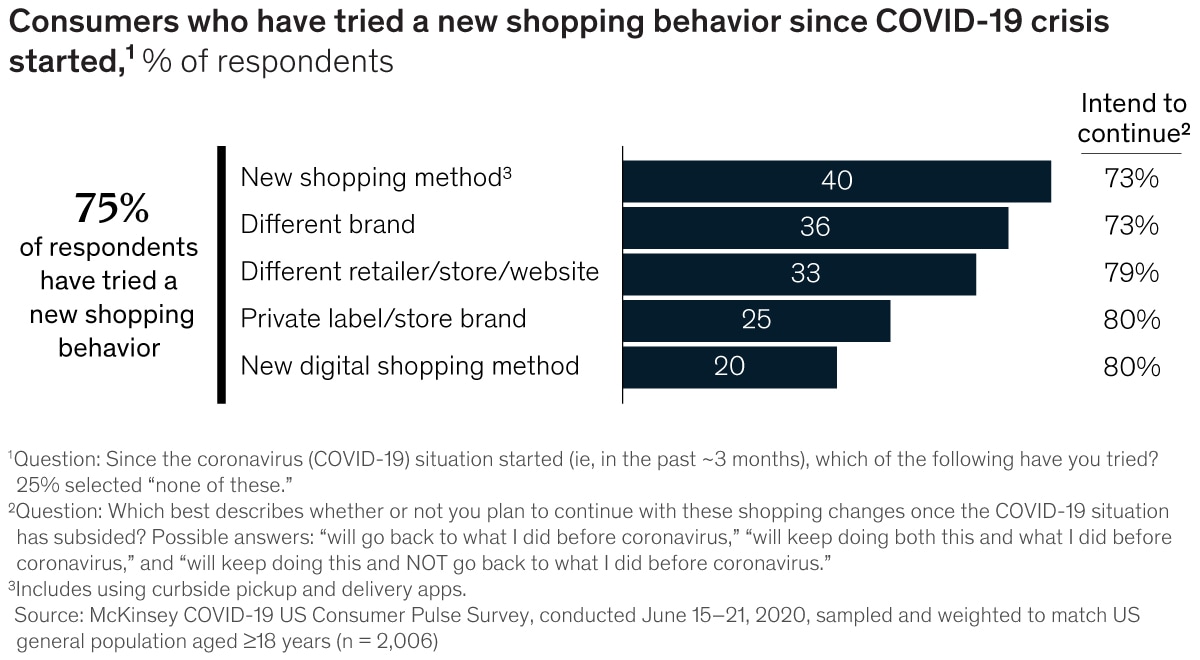

| As the global pandemic changes consumer priorities and concerns, shopping habits are changing, too. A recent McKinsey survey reveals that 75 percent of US consumers report trying something new, such as using a delivery app or curbside pickup. Perhaps even more important for consumer companies, 36 percent of respondents say they’ve switched to different brands, and most of these customers intend to continue using those brands in the future. |

|

|

|

|

| |

|

|

| INTERVIEW |

| An Honest formula for growth |

| Nick Vlahos, the CEO of The Honest Company, talks about the changing consumer and the future of the company—a fast-growing maker of baby and beauty products. Launched in 2012 by actress and mompreneur Jessica Alba, the company began as a direct-to-consumer online brand but has since expanded into stores across the US and in Europe. “We have a connection with the consumer, and we have insights into what you’re putting on your baby’s skin, so we started thinking about what you put on your own skin and what you put on your family’s skin,” he told McKinsey. “Going from baby products to beauty products made sense.” |

|

|

|

|

|

|

| THREE QUESTIONS FOR |

| Naomi Smit |

| Naomi Smit, a partner in McKinsey’s Amsterdam office, is a leader at the McKinsey Center for Advanced Connectivity, which brings together industry and strategy expertise, technical knowledge, new research, and implementation skills to capture the value presented by advances in connectivity. |

|

|

|

|

| What are the connectivity technologies of the future? What impact will advanced connectivity have on the world, and what are the benefits? |

| The future of the connected world doesn’t just mean having the newest technologies. While high-band 5G and low-Earth-orbit [LEO] satellite constellations are important, much of the future landscape will actually be defined by the expansion and evolution of existing technologies. Think fiber, low- to midband 5G, Wi-Fi 6 (the next generation of Wi-Fi technology), and various other long- and short-range solutions. |

| Next-generation connectivity tools will enable new capabilities, like near-global coverage with LEO constellations, enhanced broadband with 5G and fiber, a scaled-up Internet of Things [IoT] with Wi-Fi 6 and 5G, and the running of mission-critical services that demand absolute reliability—for instance, video for public-safety networks that could make the difference between life and death, providing critical information in real time. |

| New technologies like cloud and edge computing will further change the architecture and widen the realm of the possible by reducing computing costs and latency. |

| What role will 5G play in other industries and markets, like manufacturing, oil and gas, retail, healthcare, mobility, and more? |

| The world’s digital connections are about to become broader and faster, providing a platform for every industry to boost productivity and innovation. Recently, we published a report quantifying the tremendous potential of advanced connectivity technologies for telcos and other industries. What we found is that enhanced connectivity across seven sectors could generate $2 trillion to $3 trillion in additional value for global GDP by 2030. |

| These value-creating opportunities could transform every aspect of our lives, including building a more personalized, frictionless in-store experience with technologies such as biometric sensors and radio-frequency identification [RFID]; using autonomous farming machinery and smart-crop monitoring in agriculture; diagnosing patients with AI-powered software in healthcare; and, in mobility, improving vehicle-to-vehicle communications to increase safety and optimize the flow of traffic. |

| How can companies capture the value at stake? |

| Telco operators, connectivity-infrastructure providers, IoT-module providers, industrials, and even industrial-automation companies all have a role to play along the value chain. However, to be successful and deliver the tremendous potential at stake, these businesses will need to tackle the challenges of value-chain coordination, use-case fragmentation, misaligned incentives, data complexities, and deployment constraints. |

| Establishing common technical and data standards may help companies introduce new reimbursement models for service providers and their ultimate beneficiaries. Companies may also start to coordinate their efforts and create more partnerships to test use cases, further develop technologies, and lobby for regulatory change. |

| However, turning all of this potential into reality depends on whether connectivity providers, end users in multiple domains, and public-sector officials can forge new models and clear away some of the barriers. Considering the value at stake, there should be enough motivation for all the necessary parties to come together. |

|

|

|

| BACKTALK |

| Have feedback or other ideas? We’d love to hear from you. |

|

|

|

|

| Copyright © 2021 | McKinsey & Company, 3 World Trade Center, 175 Greenwich Street, New York, NY 10007 |

|

|

|